If you have an annuitant who finds their gift annuity income “nice, but not necessary,” they may be interested in voluntarily giving up their right to future annuity payments. Voluntarily releasing, or terminating, their interest in a charitable gift annuity (CGA) allows the charity to access the residuum early. The charity can also count part of the released amount as a new outright gift.

Voluntary termination is also an effective way of managing the issue of a CGA that is wasting. An annuitant who is charitably inclined may agree to terminate their annuity to spare the charity the continued expense of paying the annuity from general operating funds.

Terminating an annuity is simple, and an annuitant can pursue this gift even if they were not the CGA’s initial donor. The only CGA gift type that cannot be terminated early is a CGA funded with a qualified charitable distribution (QCD) because it is expressly prohibited by law (IRC §408(d)(8)(F)(iv)(II)).

If you have a donor interested in this gift type, here are the steps to follow.

1. Formalize the agreement with the donor.

A formal agreement needs to be signed between the charity and the annuitant confirming their desire to irrevocably give up their interest in the gift annuity. A sample letter from the annuitant to the charity is available in the Appendix of PG Calc’s Charitable Gift Annuities: The Complete Resource Manual, or you may request that your counsel draft an agreement. We recommend that the document state that the date of gift is the date the termination agreement is signed.

2. Record the termination and stop future payments.

Once the donor signs and returns the termination agreement, annuity payments must cease.

If you use a vendor to manage your annuity payments, share with them the signed termination document.

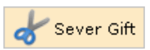

If you use GiftWrap to manage annuity payments, open the CGA’s gift record and click on the “Sever Gift” icon. This will stop future payments and change the gift’s status to “Severed.”

3. Calculate the gift value and the charitable deduction (often these values are not the same).

By terminating their interest in the CGA, the annuitant is making a new outright gift to the charity of the present value of the annuity payments they would otherwise have received over their life expectancy. The charitable deduction, however, is very likely a different value.

The IRS requires that the charitable deduction be calculated as the lesser of the current value of the gift annuity and the unrecovered investment in the contract, which is the total of tax-free and capital gain income payments that have not yet been paid to the annuitant. Because of this limitation, an annuitant who no longer receives any tax-free or capital gain income from their CGA will find themselves in the position of making a gift to charity that does not result in a charitable deduction. This does not have to sink the gift. Since only 10% of American households itemize their deductions and can therefore benefit from a charitable deduction, the donor may not require a tax benefit to be interested in making the gift.

To determine the gift amount and the charitable deduction, open the CGA case in PGM Anywhere, or if the original gift input was not saved, recreate the gift using the original gift date, gift amount, asset type, IRS discount rate and annuity rate. (Note that you will need to enter exact birthdate(s), not just age(s) for the annuitants.)

After entering all the information on the original gift:

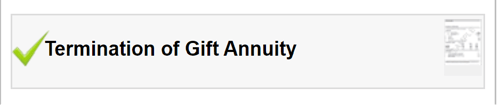

a) Within Presentations, select the Termination of Gift Annuity presentation.

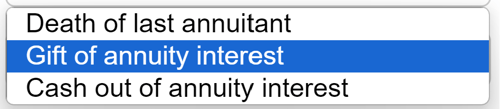

b) The Termination of Gift Annuity follow-up window will open. For “Reason of termination” select “Gift of annuity interest.”

c) Enter the date the document was signed as the “Date of annuity termination.”

d) Choose the lowest available discount rate as the “IRS discount rate for date of termination.” This choice will maximize the deduction value of the gift.

e) The resulting chart will produce three values: the Value of Annuity Interest, the Undistributed Tax-free Portion/Adjusted Cost Basis, and the Charitable Deduction for Gift of Annuity Interest. The Charitable Deduction for Gift of Annuity Interest will be the lesser of the other two values. Use the Value of Annuity Interest to book the outright gift from your donor and to steward them (see Step 7 below). Use the Charitable Deduction for Gift of Annuity Interest to draft their acknowledgement letter (see Step 5 below).

It is critical to remember that the amount released to the charity from the CGA pool is not calculated in PGM Anywhere. Either your custodian will calculate this amount for you, or if you have GiftWrap, you can run a CashTrac CGA Market Values (CashTrac) calculation to determine the amount to be distributed (see Step 6 below).

4. Determine whether the gift requires an appraisal.

While the termination of a gift annuity does release cash to the charity, it is considered a noncash gift by the IRS. If the charitable deduction is less than $5,000, the donor will not need a qualified appraisal. However, if the charitable deduction is $5,000 or more, they will need a qualified appraisal to substantiate the charitable deduction. Appraisals of an interest in a CGA typically cost less than $500, so the expense is well worth the ability to take the deduction. (PG Calc can provide this service.)

In addition to drafting a qualified appraisal, the appraiser must complete and sign IRS Form 8283, which will also have to be signed by the donor and the charity. The donor will need to submit the completed Form 8283 with their income tax and should retain copies of the appraisal and acknowledgment letter for their records. It is important to note that by signing the donor’s Form 8283, the charity is not confirming the appraised value.

5. Issue a contemporaneous written acknowledgement to the donor.

The acknowledgement for a gift of an interest in a gift annuity should state the date of gift, the nature of the gift (interest in a charitable gift annuity), and the all-important phrase “no goods or services were provided in exchange for this contribution.” Best practice is to avoid citing the dollar value of the charitable deduction, but you may wish to include a copy of the Termination of Gift Annuity chart for the donor’s reference.

6. Determine the amount of the residuum to be distributed to your charity.

Neither the Value of Annuity Interest, nor the Undistributed Tax-free Portion / Adjusted Cost Basis, is the amount that should be distributed to the charity. Rather the residuum is the amount within your CGA pool that is attributable to the CGA being terminated.

If you are working with a custodian to manage your CGA program, they can calculate this value for you.

If you manage your own CGAs with GiftWrap, you will need to run CashTrac CGA Market Values (CashTrac) to determine this amount. CashTrac is located under the Actions tab.

CashTrac is not a report. It is a computation that updates the market values stored in each gift annuity’s market value field.

To run CashTrac you will need to enter the current market value of the CGA pool, the start and end of the CashTrac period, the investment return percentage for the period, and the total payments made from the pool during the CashTrac period. The result of this calculation will update the Market Value and Market Value date for each individual gift.

Once you have run CashTrac, open the CGA’s gift record, and you will see the residuum entered into the Market Value field.

This is the amount that should be removed from your CGA pool and distributed to the charitable purpose outlined in the CGA agreement.

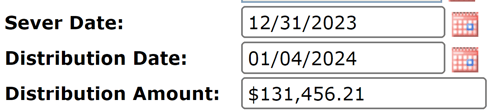

Once the distribution has been made, we recommend adding that amount to the Distribution Amount field of the gift in GiftWrap, and including the date that the funds were actually distributed.

7. Book the gift in your CRM and add it to your outright fundraising totals.

An outright gift amount equivalent to the Value of the Annuity Interest determined in Step 3 can be recorded in your CRM and added to the fundraising totals for the year. If your organization is in a campaign, this amount can also move the needle of the campaign totals.

Be careful to flag the gift for a manual acknowledgement letter so that the donor does not accidentally receive an automated tax receipt for the gift amount.

Summary

These are the operational steps to follow to ensure a smooth early release of a CGA’s residuum. However, keep in mind that this new gift is another opportunity to steward your donor. We encourage you to send a stewardship letter to the donor confirming that the gift was used as outlined in the gift agreement and thank them again for taking this bold action. If they respond favorably to this stewardship, consider asking them to be profiled on your website or in your charity’s newsletter discussing how the termination of the CGA allowed them to see their gift go to work right away. This may inspire other annuitants to consider this gift or others like it.

Submit a Comment